Buying a Home in Colorado: Is it a Good Investment in 2024?

This website may contain affiliate links and we may be compensated (at no cost to you!).

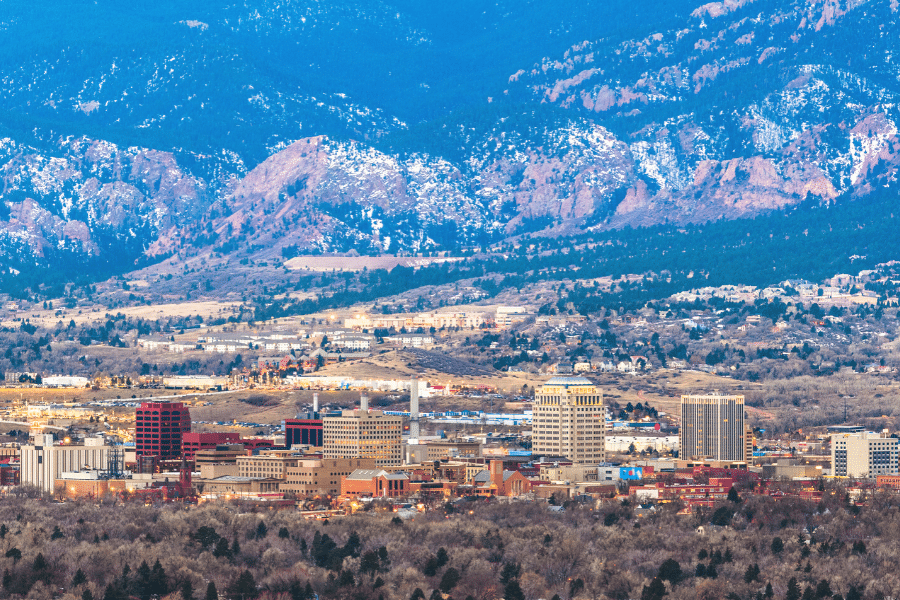

In the current market, housing prices in Colorado can be quite shocking, especially if you are moving here from another state.

It feels like you get so little square footage for the money. And we totally get it as this was one of our concerns too.

Since Carrie comes from a small town in Texas, she feels that we could have bought a mansion with the housing budget we had for our Colorado home.

On the flip side, the housing prices here can seem more affordable if you are moving from a more expensive state, like California.

Whether you are a native or a transplant to Colorado, there are pros and cons you need to consider and ways to save money on customizing your home.

We recommend Gatsby Glass in Denver if you’re looking for custom glass installations or solutions for your new home or office.

If you need garage door repair Thornton or garage door repair Broomfield, we can also suggest reliable services to ensure your garage doors are in top condition.

These tips and more are shared in this guide to help you determine if buying a home in Colorado is a good investment.

Here’s what it’s like to buy a home in Colorado, from our personal experience of purchasing two homes in the state.

1. Live in an apartment before buying

As a Colorado couple, we have lived in all 3 major cities along the Front Range; Denver, Boulder and now Colorado Springs.

And each city has different amenities, housing prices, and lifestyle options.

Since buying a home is not cheap, especially in Colorado, we recommend living in an apartment first for at least 2 years.

This way you can be sure of the city and area you want to live, and have time to understand the market, before making such a large investment.

2. Housing prices are rising daily

There’s no doubt that no matter who you ask, it’s expensive to live in Colorado! And it seems to be getting more costly by the day.

There’s no doubt, it’s expensive to live in Colorado! And it seems to be getting more costly by the day.

In fact, our house has appreciated more than $100,000 in just three years of homeownership.

3. The Colorado housing market moves fast

And the market moves fast! If you find a home that you like, schedule a showing and put in an offer that same day. Don’t wait.

Our home was listed, showings scheduled, offers submitted and accepted, and taken off the market in just two days.

That is not a lot of time to figure out if you want to buy a certain home or not.

You have to move quickly when a good home comes on the market. Don’t hesitate to put in an offer on a home you really like.

We put an offer on our house the same day it was listed, and it already had multiple offers.

4. Use an online mortgage calculator

An online mortgage calculator is a fast and easy way to see how much house you can afford.

Doing a quick Google search will yield some really simple online mortgage calculator results.

This is a good baseline for seeing what you can afford, and can give you a good starting price range for looking at homes.

But it’s important to know that an online mortgage calculator won’t include everything.

When we first used a mortgage calculator it gave us a budget of $700,000 when in reality we ended up only having a $300,000 budget.

If you are self-employed, or if you own a business, an online calculator won’t take these quirks into consideration.

5. Budget for additional costs

Speaking of budget, when buying a home you can be sure that unforeseen expenses will pop up.

Besides paying the interest and principal on your mortgage, here are some additional costs to add to your budget when buying a home.

- Private Mortgage Insurance (PMI)

- Real estate taxes

- Home insurance costs

- The cost of upkeep & maintenance

- Moving expenses

- Small repairs to comply with city codes

- Custom upgrades to the home

For example you may need to replace the roof if it won’t pass inspection. Starting with a free estimate from Mighty Dog Roofing in Boulder, Colorado is a smart first step.

This way you can see how much additional cost repairing or replacing the roof might be.

6. Get pre-approved for a mortgage

If there is any advice I can give you when buying a home these days it’s to get pre-approved for a mortgage.

In order to even start the house hunting process, you will need a pre-qualification letter, or pre-approval letter from a bank.

This paper will show how much the loan will be for, the interest rate, and the expiration date for these terms.

In Colorado, it is basically a requirement to be pre-approved before starting the home searching process.

You will know exactly what you can afford because this is the amount the bank is going to give you for the loan.

Plus, sellers really like working with buyers who are serious. If you are already pre-approved for a mortgage, your chance of sealing the deal will be much higher.

The best time to get pre-approved for a mortgage is about 30-90 days from when you hope to buy a home.

Be prepared to answer such questions like how much debt you have, what your credit score is, how long you’ve been in business, and other financial details.

7. Compare your options online

When starting the home buying process, we recommend comparing your options online. Get pre-approved for a mortgage at several different banks, to compare the rates, terms, and offers.

It is easy to start an online application at a bank you are already a customer with. It’s also a good idea to get quotes from a local credit union or community bank.

They will usually be more flexible than big banks and have better rates and features for your loan.

Don’t get discouraged if a bank doesn’t give you a high enough pre-approval amount. Just keep getting quotes and working with different banks until you find one that will work with you the best.

When buying our house, we went to multiple banks and got approval letters for amounts from $160,000 – 350,000. So, don’t give up on just one quote!

8. Save up a down payment (to avoid PMI)

Obviously, you want to save up as much of a down payment as possible when buying a home in Colorado.

A down payment will help your monthly payment become more affordable, but it also helps avoid additional costs like Private Mortgage Insurance (PMI).

PMI occurs when your home has a loan that is more than 80% of the value of the home (called a loan-to-value ratio).

A Private Mortgage Insurance company will step in and cover the remaining 20% of the home until the loan-to-value ratio is reduced.

For this reason, the recommended amount for a down payment is 20% of the total cost of the home.

But this can be a lot of money, especially considering the average cost of a home in Colorado right now is $526,779 according to Zillow.

You can get a home with as little as 3.5% down with an FHA loan, but you will have to pay PMI.

9. Utilize an escrow account

The most common way to pay for PMI is to have it rolled into your monthly payment and put into an escrow account.

An escrow account is a savings account that is managed by your mortgage company.

It takes a portion of each month’s mortgage payment and saves up money to cover things like, real estate taxes and insurance premiums.

In addition to prepaying real estate taxes and homeowners insurance, we paid an additional $163 a month for PMI on our first home.

When buying our second Colorado home, we were able to put down 20% from the proceeds of selling our first house.

Otherwise, we would have had to pay around $740 per month for Private Mortgage Insurance!

So, take that into consideration when you are budgeting for buying a home.

10. Vet multiple real estate agents

In order to find a realtor who is the best fit you may have to vet multiple agents. Don’t just go with the first one because it’s convenient, or if they are a friend of a friend.

Find out if they have the right credentials. Check to make sure they have a valid license and/or are working with a reputable firm in Colorado.

If you are unsure, a quick online search can provide a lot of the results you’re looking for.

To become a licensed real estate agent in Colorado, you must complete pre-license education, and pass the state real estate license examination.

We went through 3 real estate agents before we found the best one for our situation. Since we didn’t live in the city where we bought the home, we needed our agent to be our advocate, and help us out a lot.

Try multiple real estate agents and don’t be afraid to test them out. Don’t commit if it’s not working, as it needs to be mutual for everyone involved.

11. Work with the right realtor

Make sure your realtor has enough time for you and your needs. Do they arrive at showings on time? Do they communicate with you quickly?

As you know, the Colorado housing market moves fast and you need a realtor who moves fast too.

Find a real estate agent who will help you stick to your budget. Don’t let them take you to homes that are out of your budget, or persuade you to spend more than you’re comfortable with.

Seriously, this is the best frugal tip we could offer when looking at buying a home.

You want to enjoy your home and all that Colorado has to offer, not be house poor and can barely make the mortgage payments.

12. Do a virtual tour

In today’s social distancing economy, virtual home tours are becoming more and more popular.

If you are even remotely interested in a certain home, aim to take a virtual tour of that day, or the next day. Even if you live in a different city, or different state you want to move fast.

See if a friend or family member can give you a virtual tour of the place. Or even ask your real estate agent to do a tour for you.

Because we lived 2 hours away from Colorado Springs when we were house hunting, we asked our parents to tour the home and give us their feedback.

With the tech advances we have today, FaceTime and other ways to get a virtual tour completed so you can view the home quickly.

13. Look at mortgage assistance in Colorado

Colorado residents have several options for mortgage or down payment assistance.

One of those is getting mortgage assistance through CHFA (Colorado Housing & Finance Authority).

CHFA offers potential home buyers different programs and grants that help with down payments and closing costs.

You may also be able to get down payment assistance through a Colorado community bank.

For our situation, we could get help with the down payment and simply repay it from future profits when we sold the house.

Military families or vets can also get help with down payments, or even no-down-payment options.

Just check out the Colorado Resource Portal for Vets for more information.

14. Have an Escalation Clause

An Escalation Clause is a section that’s included in your offer when you draft up an official offer to purchase the home.

You’re basically saying that you want to escalate the negotiation process by offering a capped amount of money.

This reduces the amount of back-and-forth from other potential buyers and the seller.

You are offering a certain amount for the home, but if the seller receives a higher offer you’re willing to go up to that capped amount in order to win the deal.

In our case, the home was listed for $272,000 so we offered $276,000 but included an Escalation Clause stating that we were willing to go up to $281,000.

Another couple offered $277,000 but since we had the Escalation Clause we beat out the other offers and the seller accepted!

If we didn’t have this clause in our offer we might have lost out on the house by only $1,000.

15. Consider the time of year

The time of year determines a lot in housing prices in Colorado.

Spring and the end of summer are popular times of year for buying homes, and there is generally a lot of inventory to choose from.

However, this also means there is additional competition to worry about and the possibility of paying higher housing prices.

During the winter, you may have less inventory available but less competition from other buyers.

You may be able to get a better deal depending on the time of year you are buying a home.

16. Subscribe to a notification list from your realtor

Get alerted quickly by subscribing to a notification list from your realtor.

Most real estate firms will have an online portal or notification list you can view that displays new homes listed daily.

Or at the very least, use real estate apps like Zillow or Realtor and sign up for their email alerts.

In addition, use more than just one real estate website, as some listings are on one site and not the other. You don’t want to miss out!

17. Get an extra $10,000

If you are looking for a tax-free way to get an extra $10,000 for your down payment, consider withdrawing it from your Roth IRA.

If you have a Roth IRA you are allowed to withdraw up to $10,000 without paying taxes or penalties for your first home.

The rules are flexible though for the term “first home”, since you’re considered a “first-time homebuyer” if you or your spouse have not owned a principal residence in the past two years.

So, this is great news if you have rented an apartment for the past two years or more!

This is why we suggest moving into an apartment for two years when first moving to Colorado so you can take advantage of this withdrawal.

Another stipulation is that you must have had the account open for five years, before withdrawing the $10,000 for a home.

So keep that in mind if you need an extra $10,000 for a down-payment or even home improvements.

18. Prepare for closing day

Closing day is usually scheduled 30 days after the offer has been accepted and the property is put under contract.

During this time it can feel like you have a second full-time job!

Expect to get a lot of closing-related tasks, from getting the home inspected, to making requests for repairs, and getting the city’s appraiser to sign off on the deal.

You will also have to provide documentation of how much income you earn, and tax return information for the past several years.

It can be very time consuming and everything needs to be done in a very timely manner.

So, be prepared for this as part of the home-buying process.

Is buying a home in Colorado a good investment in 2024?

Having said all this, is buying a home in the Colorado a good investment this year?

We believe that the answer is, yes! In the current market, housing prices continue to rise pretty rapidly. And the sooner you can get in the market, the lower price you’ll pay.

When we purchased our first Colorado home 5 years ago, we paid $274,000 and this year we sold it for $415,000. That’s quite a HUGE increase in prices in just a handful of years!

But there are some Colorado cities that are still one of the top 10 cheapest places to live in Colorado.

Colorado’s popularity is also continuing to spike with no signs of slowing down.

In a few years your home’s equity will increase and you can sell it to make a decent profit.

The job market is on the rise, and people are moving to the state in droves, with more coming every year.

Not only that, but real estate taxes are much lower than a state like Texas, mostly because Colorado has a state tax. So, this can affect the cost of your mortgage payment in your favor.

In the next 5-10 years we expect that the Colorado economy will continue rising, due to the fact that more houses are built every single day.

The local government continues to do upgrades on the roads, and improve the cities to make room for more residents.

There are not many indicators that the housing market is slowing down, so get in now while you can!